Thought to run the restaurant? Don’t forget the analysis of financial data, break-even point and the risk.

Apr 23, 2021

Share

Many entrepreneurs especially a new face started the idea from passion and hope to make money and profit. Without a good idea this would be hard and take long time to pay back or else misleading to no worth of running business.

When asking about “cost that will return on investment”, what needs to be done is to analyze the financial data and estimate break-even point before opening a restaurant. Each of restaurant will use different volume of investment depending on size and nature of business. Makro HoReCa Academy has summarized lessons of Ajan Seth, Setthapond Padungpisut, Managing Director of Genosis Co., Ltd., specialist and consultant in business finance management, business valuation, strategic planning and franchise system for preparation guidance as follows.

What is ‘Break-Even Point’ and benefit of it?

Benefit of break-even point Helps entrepreneur to know quantity capability of cost and sales in term of profit

Break-Even Point is the point at which the revenue is equivalent to cost or the revenue equals to expense, a point of sales that does not lose, but it is not profitable. Benefit of break-even point analysis helps restaurant entrepreneur to know how much volume of cost and sales they need to predict the number of profits including range time of return on investment, to see and confirm on investment of business startup or to modify business plan for better profit and time of return on investment as their expectation.

Determination of investment volume and primary investment volume estimation

Expense or investment to run business as restaurant bases on assumption or information review to note volume of each investment, as such many things to be detailly counted, as fixed cost which is rent, investment restaurant operational expense, fund circulation etc. We suggest entrepreneur to set up assumption and find out information to be estimation of primary volume of investment as follows. Rent, building design, decoration cost, materials and tools, business category of business, number of employee wage, and so on are accounted as part of determination of investment.

1. Building rent and deposit, many peoplemay have concern about monthly rents but forget the case of renting place for business that owner of the place usually requires deposit in advance. This should also be included in business investment as well.

2. Decoration design other publication expenses, expense of decoration design can be estimated as minimum with advance for comparison, for gaps of approximate budget adjustment with store publication expense like menu, other publication.

3. Construction and interior expenses depend on form and style of restaurant for example, type and quantity of materials, construction and decoration expense.

4. Kitchen equipment expense ซึ่งdepends on style of restaurant service

5. Service equipment expense such as table, chair, dish, bowl, spoon & fork, glass, serving tray, different types of fabrics etc., with no difference to Dine In restaurant that focus on delivery makes not much spending on this section.

6. Media expense regarding to model of marketing plan such expense of label, tax label, online media etc.

7. Raw material to inventory expense for opening preparation of food and beverage

8. Relative license request fees such as alcohol and tobacco selling license from excise, food license and so on

9. Human resource expense such as employee wage since preparation period, training expense

10. Utility expense such as water bill, electricity bill, telephone bill, internet etc.

11. Extravagant equipment material expense means expenses incurred with disposable items such as pen, paper, store appliances etc.

12. Reserve working capital is to be used for debt and expense to circulate for the business to continue which may not be part of in equipment asset, but as emergency reserve for sufficient usage at least 3 – 6 months.

13. Fee of registration and company

14. Operating expenses at least the first month

Return on Investment (ROI)

For restaurant investment, if we knew how to get information of return on investment or ROI as a calculation of net profit dividing investment and multiplying 100, e.g.

Let’s say our monthly profit is 280,000 baht

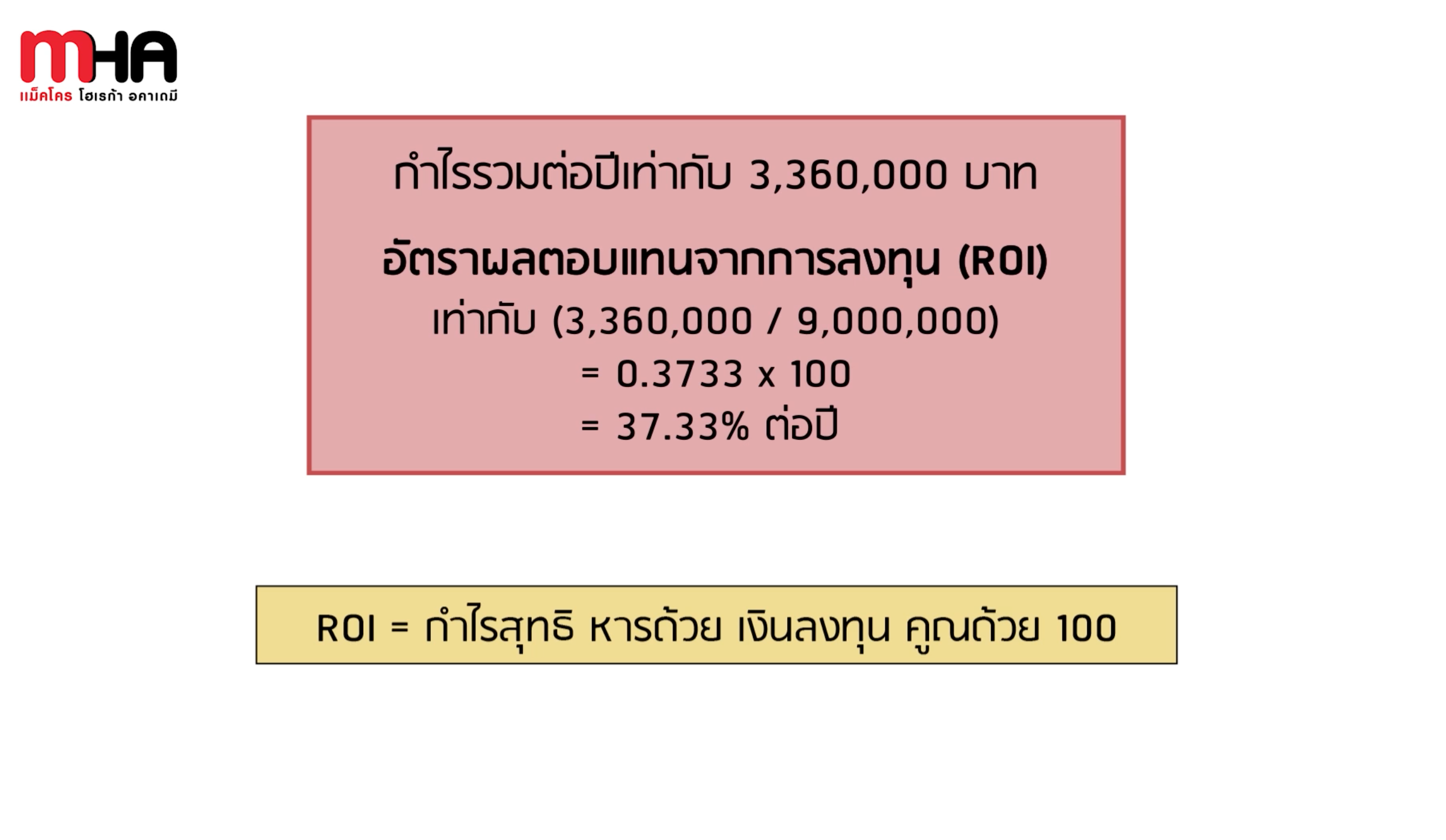

Means that annual profit (x12) is 3,360,000 baht

Divide total investment of 9,000,000 baht and multiply 100

The result of ROI is at 37.33% per month

This means that in case of investment to this restaurant get return on investment from restaurant operation at 37.33%as a result of deducting total expense. Many people may have questions in their mind that “how much the ratio of return will be enough”. As consideration at this point to think of a case of How much percent of interest do we have to deposit to bank with the same amount of money or invest in other forms? Comparison to see return on investment with the same amount of money turns out satisfying for earlier investment. Less number of customer visit lessens ratio of return according to expectation show the risk for entrepreneur of restaurant investment.

Total annual profit = 3,360,000 baht

Return on Investment (3,360,000 / 9,000,000)

= 0.3733 * 100

= 37.33% per year

Return on Investment = net profit divides investment and multiplies 100

How to know break-even point and time of return on investment

As mentioned above, break-even point is the point at which the revenue is equivalent to cost or income perfectly equals to expense, when we have found the total investment, those fixed costs of building restaurant and working capital from budget that has been set will show us the volume of investment of restaurant which will be calculated for range of time of return on investment by dividing investment amount with monthly net profit.

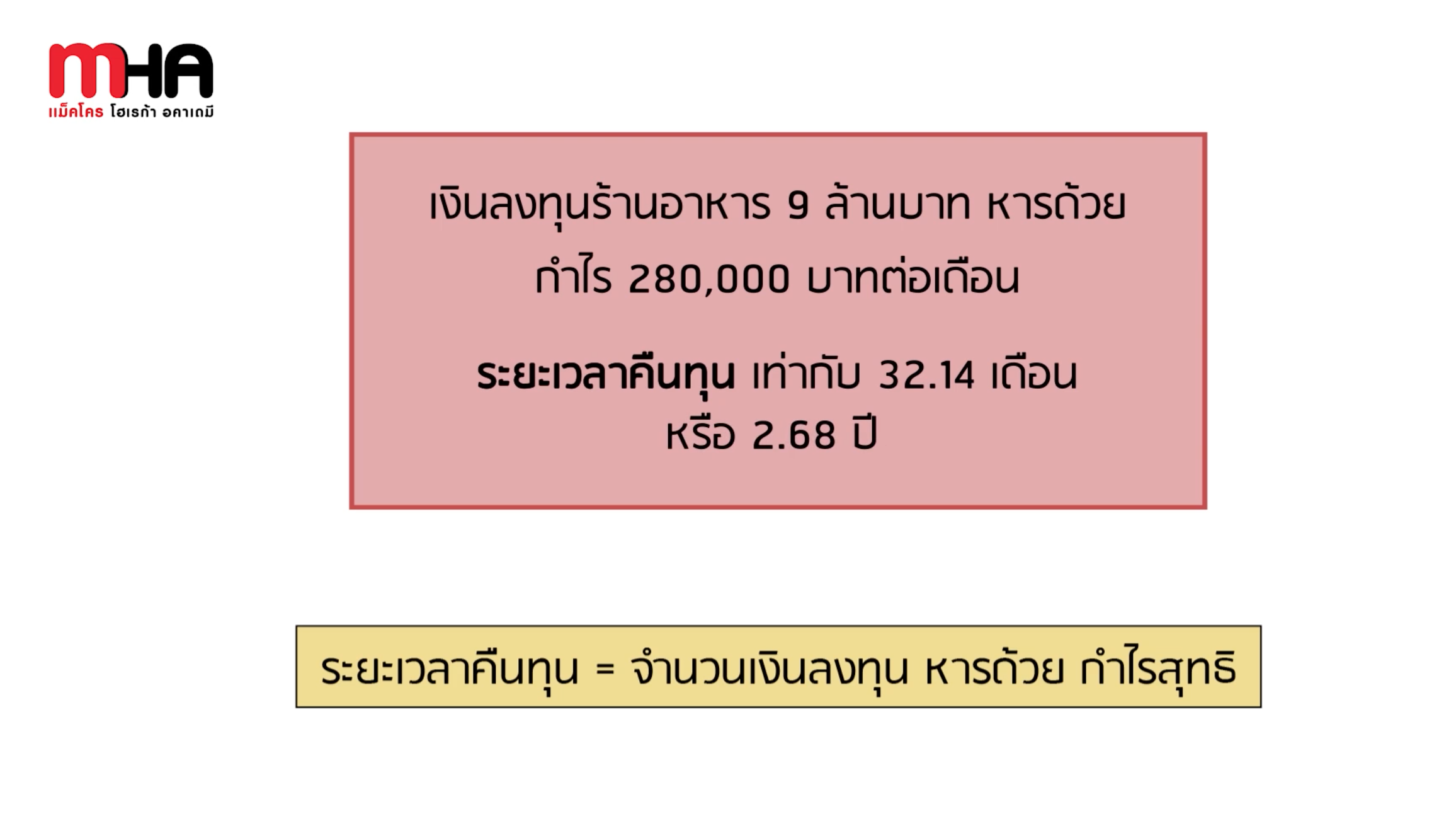

For example, total investment was 9 million bath is divided by profit of 280,000 baht per month incurred time range of return as 32.14 months or 2.68 year and so forth.

Volume of restaurant investment = 9 million bath divides profit, 280,000 baht per month

Period of return on investment = 32.14 months or 2.68 years

Period of return on investment = investment amount divided by net profit

From the mentioned example, if we ran a restaurant with investment value of 9 million baht, rate of return as analyzed is ROI of 37.33% per year and will be given back approximately around second year of business (2.68 years). This returns to ask yourself that “are you satisfied with return rate number and period of return?”, if yes, you just follow the business and investment plan that have been laid. But if the answer is “dissatisfied”, we have to continue analyzing how fast we want for the return which we need to find the way to reduce some parts of investment budget without any effect to business plan that it has been already analyzed.

‘Net Cash Flow’ and ‘Net Present Value’, things that must know

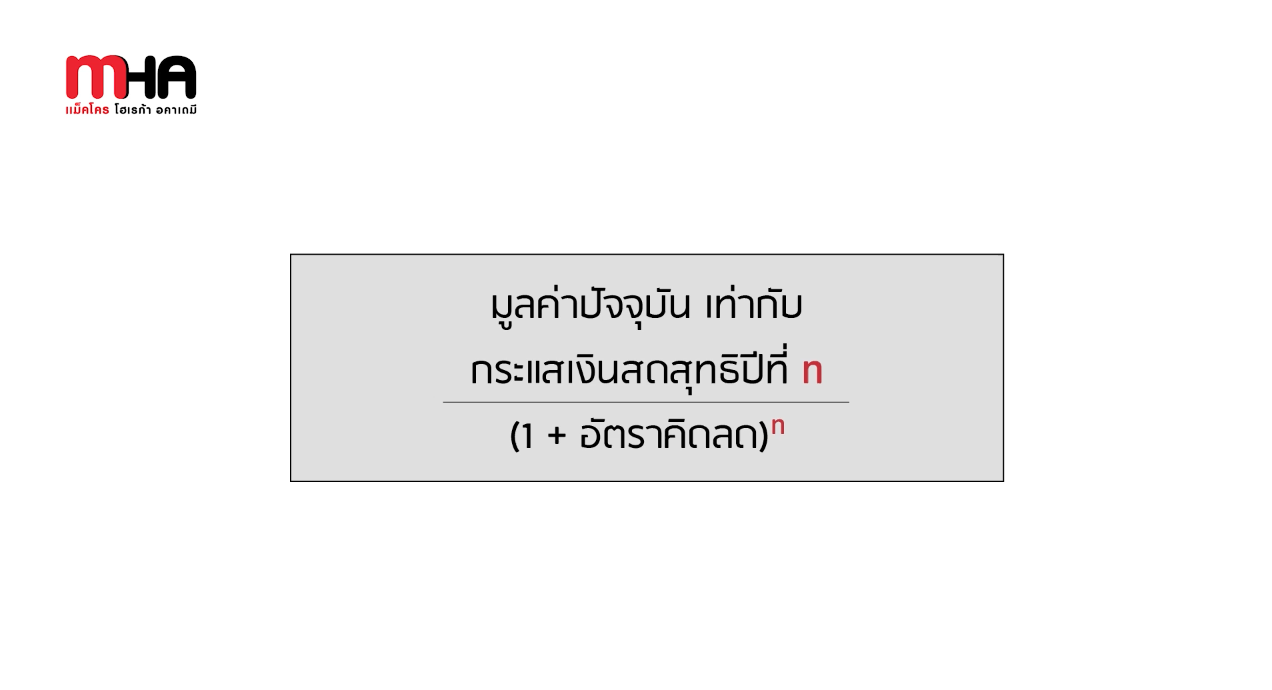

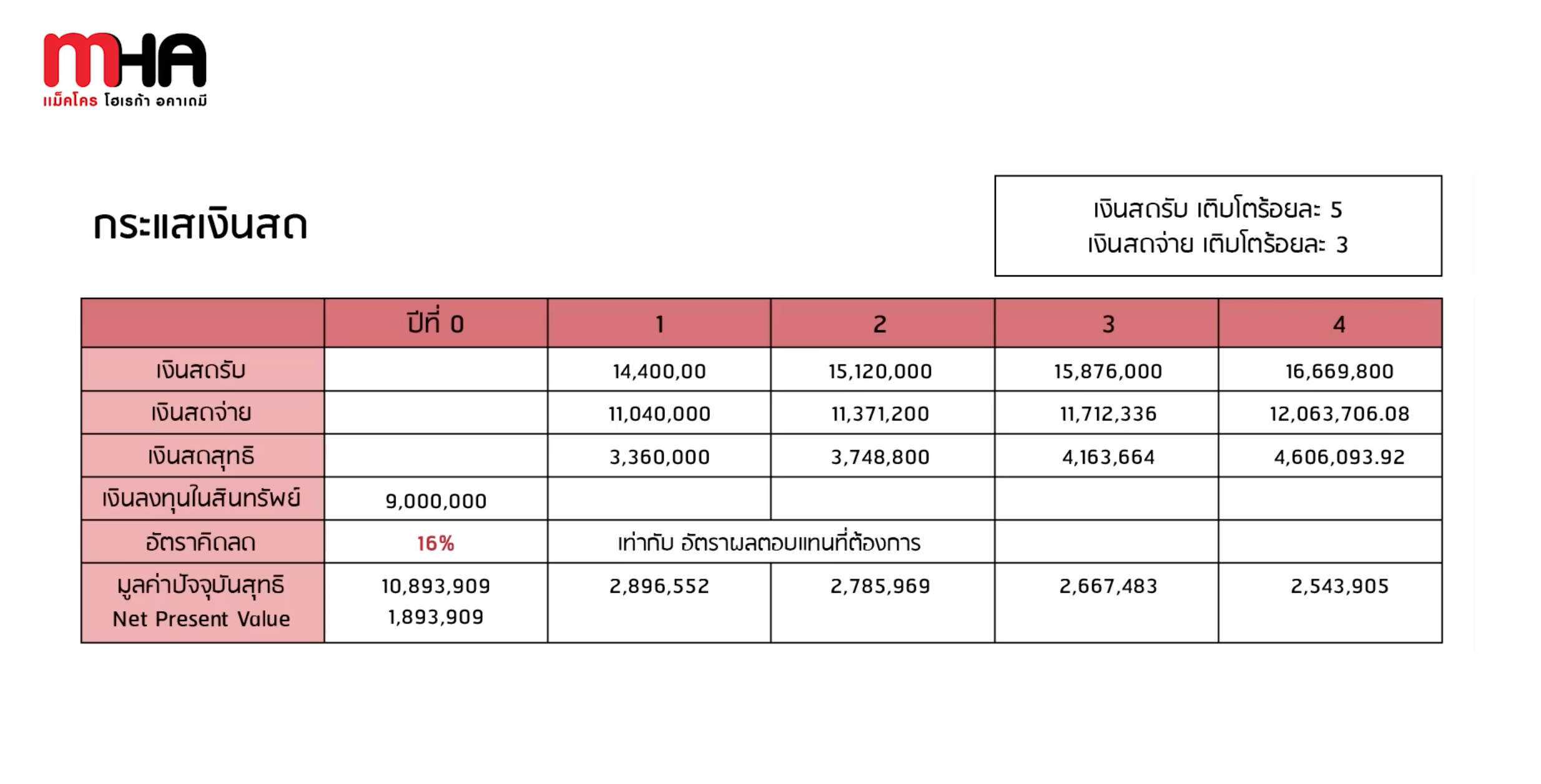

The important thing that entrepreneur must keep in mind from planning accounting is even we have planned for accounting and finance to know how much money and how much profit will be returned in the future, but currency value in different time may not always be the same because of currency value change, which will continuously decrease. Therefore, we need to find ‘New Cash Flow’ to find ‘Net Present Value or NPV’, difference between total present value of net cash flow over the project lifetime and present value of investment used any ‘discount rate’ to adjust the value of cash flow generated in different intervals to be at the same point which is at present.

NPV > 0 efficiently invest, the return on invest is greater

NPV = 0 cover expense, consider from other factor rather the finance

NPV < 0 avoid, the return on investment is less

To find net present value for analyzing range of time is benefitable that money we will receive in the future as present value and compare with present volume of investment, found the return rate in the future that we have invested will actually benefit or not.

To consider that this restaurant business is worth to investment or not, follows formula and example below, this can be said complicated which beginner would have taken some time to understand.

Therefore, we would like to recommend online course by Ajan Seth, Setthapond Padungpisut, of restaurant business possibility study which content in this section is a part ofChapter 5: Analysis of financial possibility and Chapter 6: investment case study. We guarantee that this will benefit every entrepreneur who join the class, Click for Free registration! >> http://bit.ly/3a5tOUM Present value = Net cash flow year “n”

(1+ discount rate)n

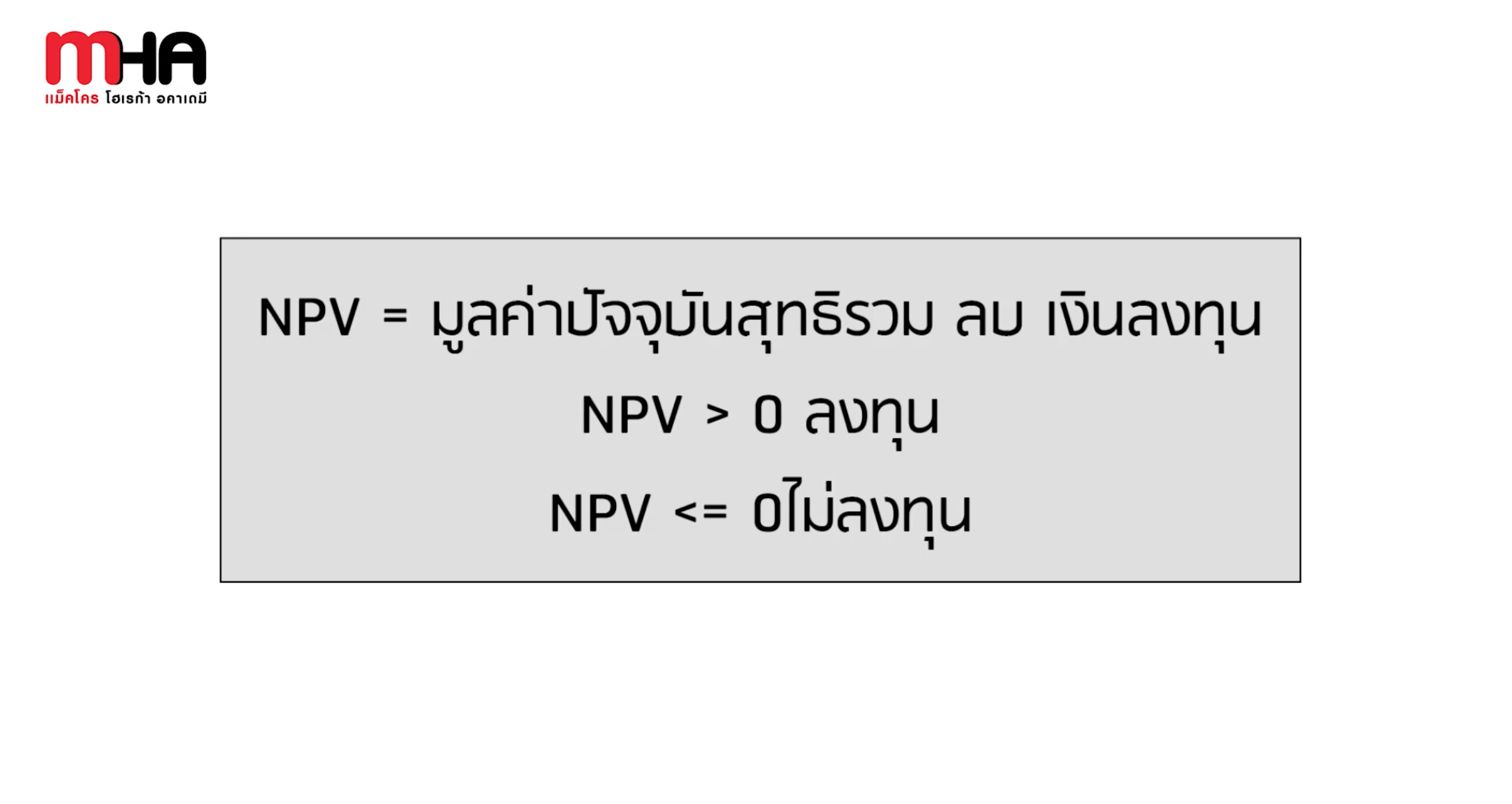

NPV = total net present value - volume of investment

NPV > 0 invest

NPV <= 0 not invest

Advantage of Financial Data

Help making decision easier

Form to data analysis shaping business plan for satisfying profit and period of cost return

Shape data and hypothesis in the view of better reward for example, investments or expenses may reduce (minimize quality) or find the way to get more customers without cost of additional service and so forth.

To analyze information and establish operational strategy, which will be very useful to notify any change for the competition as beneficial and expected result.