Jul 15, 2020

After the easing of the Covid-19 control measures, many businesses have started to recover. The degree to which they recover differs between businesses. Restaurants, which started opening their doors to welcome customers, are no exception.

After the easing of the Covid-19 control measures, many businesses have started to recover. We believe one of the issues people are worried about is probably money. It would be good if we could have a guru give them some advice about how to plan and improve the formula for their financial management system. Chakkraphong “Coach Num” Mesaphan, or Num the Money Coach, is a financial guru who will share his ideas and techniques for managing working capital and debt and how to apply for credit so restaurateurs can use them to recuperate and survive on the long term.

- Working Capital, the Heart of Financial Management That Restaurateurs Need to Know

- How to Manage the Working Capital

- Lay Out a New Financial System to Recover the Business

- How to Look for Credit as an Alternative for Recovering from the Financial Crisis

- How Should Good Debt Management Be Done?

Working Capital, the Core of Financial Management Restaurateurs Need to Know

Whether it’s a good business or other kinds of business, working capital or cash flow is essential. It’s the first thing Coach Num mentioned need to be considered in financial management when businesses are affected by the Covid-19 crisis, so he wants every business to think about it seriously.

Coach Num explained that, when doing business, people tend to look at the profit. In management, however, they have to look at the heart of it: working capital. People have to ask themselves what can cause a business to fail. It’s not losing money, but insufficient working capital. Although you might lose money, the business could continue if you have cash in your hands.

Working capital can come from several channels, including profit, loans and use of the money customers pay in advance such as for pre-order products, for other things first, etc.

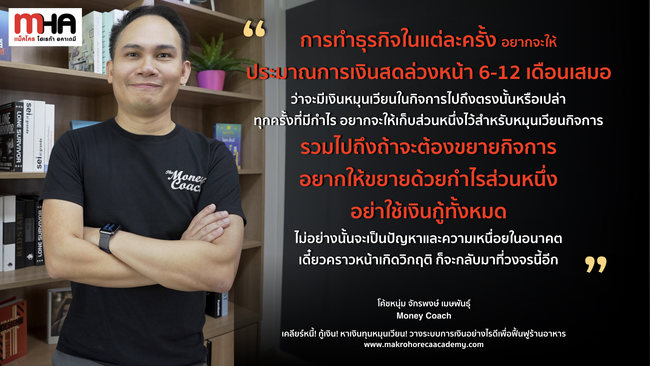

Therefore, the first suggestion is that working capital is the number-one goal you have to always check and maintain. Successful businesspeople are those who always make sure they have enough working capital for the next 6 – 12 months and, even better, the working capital should come from the profit. That’s what will really make a business survive.

How to Manage the Working Capital

What people should think about during a situation like this is, if your restaurant has working capital in hand and how you should manage it.

Concerning the issue above, Coach Num advised that, at times like this, people should try to keep cash on them for as long as possible and prioritize ‘essential spending’ and buy things they really need to circulate, for example, ingredients and employees. These are essential things for running a business. Save your money on other things for now and negotiate with trade payables for materials, equipment and rent. If you can negotiate with them, then try. Pull the cash in a bit. Pay with a little credit. As for marketing, check carefully whether it’s worth the payment.

“Right now, you should have about 6 months’ worth of working capital because, from the looks of it, this could last until the end of the year. So, if you want to add a little cash to circulate in your business, you might have to make sure it’ll last 6 months. However,

if that’s not feasible, or if your business is still able to sell, you might only have to add enough for about 3 months, although you might have to work hard. And you have to think about what can make the funds come back quickly, for example, new product styles, new dishes and new products.”

Lay Out a New Financial System to Recover the Business

After the introduction of Covid-19, a lot of businesses today are in a pickle. Thus, if you want to recover your business and keep it running, Coach Num is inviting you to inspect your own business again, especially the financial aspect, which is the main factor that can either make or break your business. The two aspects you should check are as follows:

- Liquidity What you have to watch is expenses. Watch your current expenses. The financial aspect is separated into the following two parts:

- Operational Expenses - Businesses have operational expenses such as employee wages, rental fees, ingredient cost, etc. We believe entrepreneurs know very well what they have to reduce, but we want you to realize first that you shouldn’t reduce the number of employees because they’re rather hard to find during the recovery period.

- Expenses from capital or debt. We want to really emphasize that in times like these entrepreneurs have to be diligent about going to their creditors to negotiate about parts of the debt that will relieve your burdens immediately. (Suggestions for debt management are in the next section.)

- Pull in Cash A mantra you should memorize is, don’t go take out a loan, yet. Be patient. Your business isn’t stable yet. If you take out a loan, it’ll be even worse. You could find a similar alternative and adapt to it. For example, instead of selling as a small business, some places are starting to tie their businesses in with a company, resulting in high sales figures and offering delivery along with designing new dishes to generate cash. One essential thing is you have to use the resources you have to the fullest. Some restaurants use their receptionists as deliverers. These days, you might have to transform everything while picking up other things on the side.

Moreover, you have to make plans for the next 6 – 12 months in advance so you can see your own situation. You also have to check it every month to make sure you’re operating according to plan. You have to do everything carefully, thoroughly and in a disciplined manner.

How to Look for Credit as an Alternative for Recovering from the Financial Crisis

If you’ve reduced your expenses and increased your income, and it’s still not enough and you’re sure your business still has a future, you might have to eventually enter the credit system to use it to continue your business.

As for credit application, Coach Num has some interesting advice. He pointed out that in “believing your business has a future”, you can’t just make assumptions. You need to rely on estimated numbers. For example, if everything is back to normal, how much income do you really have? Where does it come from? How is it earned? Only then can you plan on applying for credit. When applying for credit, the items you have to evaluate are as follows:

- Don’t use the wrong type of credit. When in big trouble, a lot of people choose credit cards to keep their businesses running. This is very dangerous since the interest is very high at 20% and up. You could lose all your profits this way. This type of credit is used to keep the business afloat, but it doesn’t revive it. Therefore, never do this and never go outside the system.

- Use low-interest credit from financial institutes. There are a lot of special credit types. If you want to apply for credit with a bank, make sure to visit a lot of different banks because they have a lot of injected policies to help you out, such as interest rates under 2%. Now, when you go in, don’t be alarmed if the bank teller tells you that the credit is out. Just ask if they have anything similar. If the interest rate is 2.5 – 3.5%, we believe it should be acceptable. Also, don’t ask for just the percentage. You should deal with the actual numbers. For example, if you took out a loan of 1,000,000 baht, how many installments would you have to make? What’s the interest? Then compare all of the interest rates.

- Don’t take out random loans with no repayment plan. You need to prepare a repayment plan. You have to figure out how much you have to pay back per month and put that figure into your budget to see if you can pay it back. If you’re unable to pay it back, extend the time, so you have to make smaller installments.

How Should Good Debt Management Be Done?

As Coach Num has already advised at the beginning, entrepreneurs now have to go to their creditors to negotiate. Coming to a compromise can help lighten the load a lot. Ways to negotiate with creditors are as follows:

You have to negotiate openly and honestly. When negotiating with a financial institution, you should go in with your profit and deficit figures to clearly show them that money isn’t coming in and that you’re really in trouble. Show them what will happen over the next 3 – 6 months if you continue to lose money. Show how this method can help you. You’ll usually get good terms.

Do your homework beforehand. A big challenge in negotiation is you have to do your homework first. You have to think about where you want to negotiate. There are 5 main options for this: 1. The best option is to suspend all your payments; 2. Pay only the interest; 3. Reduce the interest; 4. Request an installment reduction; 5. Turn short-term loans into long-term loans. This is how you reduce to survive. It gives you options. Don’t let the financial institution be the only one presenting options. They don’t know if you’re going to survive and it would just fail in the end. Therefore, try negotiation for the five abovementioned terms. We believe it can help you keep things going.

Suggestions and Encouragement

Lastly, Coach Num wants to leave us with some advice for running a business during the Covid-19 crisis: If your business can recover from Covid-19, he wants people to remember it as a lesson. A lot of businesses clearly don’t have a backup fund and don’t check their cash estimations. In addition, when their businesses grow, they tend to hurry up and expand them. A lot of times the expansion is done using credit which creates a hidden burden that they don’t see when they’re selling well. However, if they start losing business, debt usually pops up as a problem.

“I want to advise everyone that, if you get through today’s crisis, never forget it. Each time you start a business, I want you to always estimate how much cash you’ll need for the next 6 – 12 months, so you’ll know if you have enough working capital to get you there. Every time you make a profit, I want you to save some of it as part of the circulating funds. Also, if you need to expand your business, I want you to use your profits as part of the funding. Don’t use loans for everything. Otherwise, it’ll become a problem and exhaustion for you in the future. Next time there’s a crisis, you’ll just be back in this cycle. In the end, you’ll have put the work in and not get any richer.”

“Entrepreneurs work hard because they have to take care of a lot of things all at the same time, whether it’s customers or employees. I want to say that every problem has a solution. In times like this, you have to use your senses and diligence in deciding to fight. Particularly when it comes to finances, don’t make hasty decisions. Every time you make a financial decision, other than figuring out where to get the money, you have to ask yourself if, after getting money, there are any long-term consequences or burdens that can cause problems. In order to answer this question, you have to go back to your cash estimations, which you should prepare in advance, so you can see the facts before making your decision. In addition, I want to encourage to you be patient and fight a bit, because this situation will pass one day. I believe it will pass if everyone use their senses and spirit in solving their problems.”